The complete guide for fintech professionals and content creators: how AI agents are transforming cross-border loan origination, KYC, AML compliance, FX risk management, and loan servicing at scale in 2026.

| $4.3T Global CB Loan Volume (2025) | 52% Fewer Processing Errors | 38% Faster Transactions | $3.50 ROI per $1 Invested | €35M EU AI Act Penalty Cap |

Table of Contents

1. What Are AI Agents for Cross-Border Loans?

AI agents for cross-border loans are autonomous, multi-step AI systems that manage the full lifecycle of international lending operations — from application intake and identity verification through credit risk assessment, regulatory compliance, FX hedging, and ongoing loan servicing — across multiple jurisdictions simultaneously. Unlike traditional rule-based automation or simple chatbots, these are agentic systems: they plan, decide, and execute complex multi-step workflows with minimal human intervention.

The operational shift: Where rule-based automation executes fixed instructions, AI agents take ownership of workflows. A KYC agent doesn’t just check a box — it ingests identity data, triggers AML screening, applies internal risk models, confirms policy compliance, and only advances the application when every dependency is satisfied. Low-risk cases move in minutes. High-risk cases are routed to compliance with full context attached.

Cross-border loan servicing presents unique challenges that domestic lending never encounters: multi-currency loan recalculation as exchange rates fluctuate continuously, KYC verification across jurisdictions with different identity standards, AML compliance under FATF, AMLA, FinCEN, and regional regulatory bodies simultaneously, and document processing in multiple languages. These are precisely the conditions where AI agents deliver the most measurable value.

The scale: Cross-border lending volume reached $4.3 trillion globally in 2025 per the Bank for International Settlements. AI-enabled institutions are capturing disproportionate market share of this growth — the operational efficiency and error reduction advantages compound over time into structural competitive advantages that manual institutions cannot close.

| 💡 Pro TipFor content creators covering fintech: this is not a future technology story. Goldman Sachs, JPMorgan, and major regional banks are already deploying agentic AI across KYC, AML, loan processing, and compliance reporting in production environments in 2026. The story is adoption velocity and regulatory compliance — not capability proof of concept. |

2. The 5 Core Challenges AI Agents Solve

Cross-border lending is operationally complex in ways domestic lending is not. AI agents address five structural pain points that have historically limited scale and efficiency in international loan operations:

- 1. Multi-currency complexity: A loan originated in euros but serviced by a borrower earning US dollars changes in effective value continuously as exchange rates fluctuate. Manual recalculation is impossible at scale. AI agents monitor real-time FX rates, trigger hedging actions automatically when thresholds are breached, and recalculate EMIs and repayment schedules continuously — maintaining accurate loan valuations across currency pairs without human intervention.

- 2. Jurisdictional regulatory fragmentation: A single cross-border loan may be subject to FATF guidelines, EU AMLA rules, FinCEN/BSA requirements, and local country regulations simultaneously. In 2026, the EU’s new AMLA directly supervises high-risk cross-border financial entities, enforcing a single rulebook across EU member states — transitioning from 27 national interpretations to one centralized standard. AI compliance agents ingest regulatory circulars automatically, identify affected loan portfolios, and generate compliant reports across jurisdictions.

- 3. Cross-border KYC complexity: Cross-border KYC for individual borrowers is complicated by data localisation rules, inconsistent digital identity standards across jurisdictions, varying PEP (Politically Exposed Person) lists, and different biometric verification requirements. The EU Digital Identity Wallet partially solves the identity problem. AI KYC agents handle the jurisdictional variation — querying the right identity registries, applying jurisdiction-specific EDD requirements, and maintaining audit trails that meet each applicable regulatory standard.

- 4. Multi-language document processing: A cross-border loan may involve income documentation in three languages, property valuations in local formats, and regulatory forms requiring jurisdiction-specific disclosures. AI document processing agents use OCR and NLP to extract structured data from unstructured documents across languages and formats — eliminating the manual data entry that accounts for up to 40% of loan processing time.

- 5. Cascading compliance risk: When multiple AI agents operate in sequence, an error made by one agent can become the input for the next — building a chain of flawed decisions that is difficult to trace and costly to correct. This is the key risk of multi-agent architectures in financial services. The mitigation: every agent action must produce a reason code, an audit trail, and a human-readable explanation — the EU AI Act makes this mandatory for high-risk financial AI systems from August 2, 2026.

3. The 7-Agent Cross-Border Loan Pipeline

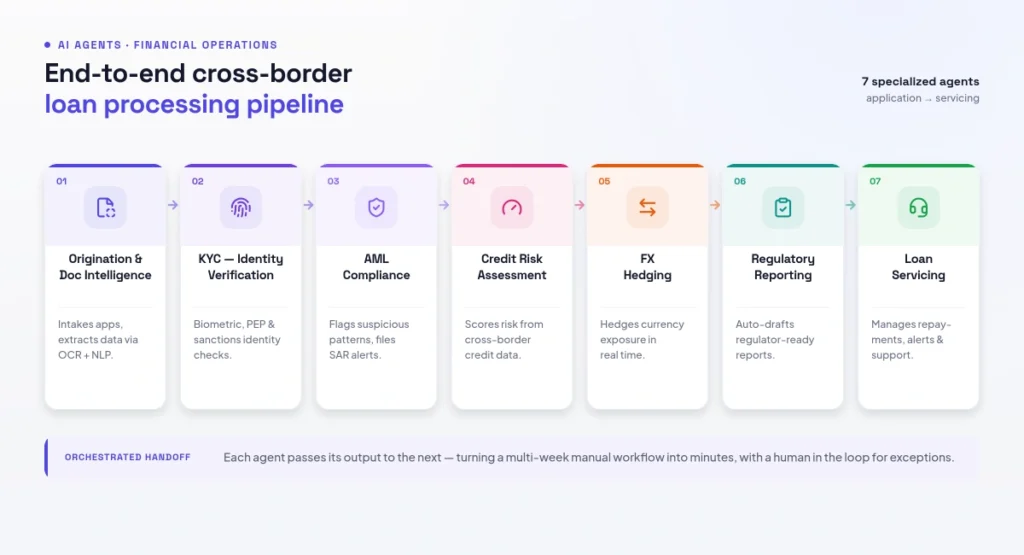

Figure 2: 7 AI Agents — End-to-End Cross-Border Loan Processing Pipeline

A complete cross-border loan processing system in 2026 typically deploys seven specialized AI agents, each owning a defined workflow stage:

Agent 1: Origination & Document Intelligence

The origination agent is the intake layer — it processes loan applications in multiple languages, extracts structured data from unstructured documents using OCR and NLP, validates data field completeness, and cross-checks submitted information against internal systems and external bureaus in real time. A single application can trigger up to 20 separate process steps; the origination agent coordinates these automatically, routing complete applications forward and requesting missing information from borrowers without human involvement. Processing time: minutes versus days for manual intake.

Agent 2: KYC Agent — Identity Verification

The KYC agent performs biometric identity verification (document scan + liveness check), screens against PEP lists and global sanctions watchlists, applies jurisdiction-specific Customer Due Diligence (CDD) requirements, and triggers Enhanced Due Diligence (EDD) workflows for high-risk profiles — all while maintaining a complete audit trail that meets regulatory requirements. At major banks, agentic AI has already transformed KYC from a week-long manual process into a largely automated workflow completed in seconds for standard profiles.

Agent 3: AML Compliance Agent

The AML agent monitors transaction patterns against customer behavioral baselines, applies contextual risk scoring that adapts to cross-border transaction spikes, screens counterparties against real-time sanctions lists, identifies structuring behavior and layering patterns across accounts, and automatically drafts Suspicious Activity Reports (SARs) for analyst review. Nasdaq Verafin’s agentic AML system reduced sanction-screening alerts by over 80% in 2025 — freeing human investigators to focus on high-value cases rather than false positive triage.

Agent 4: Credit Risk Assessment Agent

The credit risk agent queries cross-border credit bureaus, processes alternative data sources for borrowers without traditional credit histories, evaluates income stability and debt exposure across currency pairs, assesses collateral values in local market contexts, and applies underwriting rules against policy thresholds. It produces a risk-scored application with documented reasoning that satisfies both internal credit policy and external regulatory explainability requirements — critical under the EU AI Act’s mandatory transparency provisions.

Agent 5: FX Hedging Agent

The FX agent monitors real-time exchange rates across all relevant currency pairs, calculates exposure on the outstanding loan portfolio, executes hedging actions automatically when pre-defined thresholds are breached, recalculates EMIs and repayment schedules in borrower-currency terms, and generates multi-currency statements. This agent operates continuously — not on a batch schedule — meaning currency risk is managed in real time rather than reviewed periodically.

Agent 6: Regulatory Compliance Reporting Agent

The compliance agent automatically ingests regulatory circulars and notifications the moment they are published, extracts specific provisions, identifies affected business areas within the loan portfolio, maps requirements to existing products, and generates preliminary impact assessments with clause references and recommended actions. Tasks that previously required 2-3 weeks of analyst time — reading, interpreting, and mapping new regulatory guidance — are completed within 24 hours. All outputs include full audit trails and explainability documentation for regulator review.

Agent 7: Loan Servicing Agent

The servicing agent manages the ongoing life of the loan: payment scheduling, EMI tracking, delinquency detection and escalation, borrower communications in local languages, multi-currency statement generation, and portfolio monitoring for policy violations. It operates 24/7, compares actual loan performance against credit policy continuously, and flags deviations — including unauthorized exceptions and patterns of repeated policy violations — the moment they occur rather than at the next audit cycle.

| 💡 Pro TipThe most important design principle for multi-agent cross-border loan systems: implement bounded autonomy, not full autonomy. Low-risk retail onboarding can move through straight-through processing when confidence levels are high. High-risk cases — source of funds reviews, complex UBO analysis, high-risk geography reviews — still require analyst interpretation. Build explicit human escalation triggers into every agent workflow. |

4. Top AI Agent Platforms for Cross-Border Lending

| Platform | Best For | Key Strength | Compliance | Scale |

|---|---|---|---|---|

| FIS Global | Enterprise banks — full lifecycle | Massive transaction volume, multi-jurisdiction | FATF, FinCEN, AMLA | Global — all sizes |

| Kore.ai | Mid-market lenders — loan processing | 12 proven AI agent use cases, KYC + AML + underwriting | SOC 2, GDPR, RBI, SEBI, FCA | Mid to Enterprise |

| Fini | Fintech support + compliance ops | PCI-DSS L1, 48hr deploy, backend action execution | PCI-DSS, SOC 2, GDPR, HIPAA | Fintech focused |

| Temenos | Cloud-native core banking | Real-time data processing, AI-personalized products | Multi-jurisdiction native | Regional to Global |

| Mambu | SaaS lending platforms | Modular architecture, API-first, rapid market entry | GDPR, PSD2, local APIs | Growth fintech |

| Sumsub | KYC/AML verification layer | User + business verification, transaction monitoring | FATF, MAS, FinCEN, FCA | Global |

| Fenergo | Client lifecycle management | $16M compliance cost savings benchmark, KYC SaaS | GDPR, AML Directives 5+6 | Enterprise banks |

5. KYC & AML Automation — 2026 Regulatory Landscape

The 2026 regulatory environment for AI-driven cross-border KYC and AML has crystallised around three concurrent developments that every lender deploying AI agents must understand:

5.1 EU AI Act — High-Risk AI Classification (August 2, 2026)

The EU AI Act imposes explicit requirements on high-risk AI systems in financial services — including credit scoring and fraud detection — from August 2, 2026. Systems in scope must be transparent, interpretable, bias-free, and supported by complete documentation. Automated decisions must be auditable. Every AI-driven decision in a KYC or AML workflow must produce a reason code, an audit trail, and a human-readable explanation of why the outcome was reached. Penalties reach €35 million or 7% of global turnover — making compliance not optional but existential.

5.2 EU AMLA — Single Rulebook for Cross-Border Entities

The European Union’s Anti-Money Laundering Authority (AMLA) directly supervises high-risk cross-border financial entities in 2026, enforcing a single rulebook across EU member states. For lenders operating in multiple EU countries, this transition — from 27 national interpretations to one centralized standard — requires integrated, pan-European compliance programs that are consistent, transparent, and centrally auditable. AI compliance agents that can adapt to a single authoritative standard are structurally better positioned than systems built around national rule sets.

5.3 FATF AI Horizon Scan — Agentic AI in Financial Crime

The FATF Plenary of October 2025 formally approved an AI Horizon Scan covering the use of generative and agentic AI in financial crime — signalling that regulatory guidance specific to AI-in-compliance is actively in development. Regulators on both sides of the Atlantic have consistently stated that black-box AI is not acceptable in financial crime compliance. The practical implication: every AI agent deployed in KYC or AML must be explainable by design, not retrofitted for explainability after deployment.

| ⚠️ Compliance AlertThe EU AI Act enforcement date of August 2, 2026 means institutions deploying AI for credit scoring, fraud detection, or AML in the EU must already have compliance documentation, audit trails, and explainability frameworks in place. Post-deployment compliance retrofitting is not viable — the compliance architecture must be designed in from the start. Penalties of €35M or 7% of global turnover apply from day one of enforcement. |

6. FX Risk Management with AI Agents

FX risk is the unique operational challenge of cross-border lending that has no domestic equivalent. A loan originated in euros for a borrower earning US dollars creates continuous currency exposure across the full loan tenor — potentially years of FX fluctuation that must be monitored, hedged, and reflected in accurate loan valuations and repayment schedules.

6.1 Real-Time Rate Monitoring

AI FX agents monitor exchange rates across all relevant currency pairs in real time — not on batch schedules. This continuous monitoring enables immediate detection of threshold breaches and automatic hedging action, rather than periodic reviews that allow exposure to accumulate between check cycles. For portfolios with significant cross-currency exposure, continuous monitoring versus daily batch review can materially reduce FX losses during periods of high volatility.

6.2 Automated Hedging Execution

When the FX agent detects that currency movement has breached a pre-defined risk threshold, it executes hedging actions automatically within its defined parameters — without requiring human approval for routine hedging operations. High-stakes or unusual hedging situations above defined thresholds are routed for human review with full context attached. This mirrors the human-in-the-loop model that regulators expect: routine automation with human oversight at defined escalation points.

6.3 EMI Recalculation and Borrower Communication

When exchange rate movements materially affect a borrower’s repayment obligation in local currency terms, the FX agent recalculates EMIs automatically, updates loan schedules, generates revised repayment statements in the borrower’s local language, and triggers communication workflows to notify affected borrowers. These workflows maintain borrower transparency — a regulatory requirement in most jurisdictions — without requiring manual intervention for each rate movement.

| 💡 Pro TipThe ISO 20022 messaging standard is a key enabler for AI FX agents in cross-border lending. Its rich, structured data format allows AI agents to automate sanctions checks, fraud detection, reconciliation, and reporting at global scale — replacing the stopgap translation tools that many institutions used to meet the 2025 Swift migration deadline. Institutions that build AI FX infrastructure on ISO 20022 native data structures have a significant automation advantage. |

7. ROI & Performance Benchmarks

| Metric | Result | Source | Context |

|---|---|---|---|

| Processing error reduction | 52% | McKinsey Financial Services 2025 | AI-enabled vs manual cross-border operations |

| Transaction completion speed | 38% faster | Bank for International Settlements | Across AI-enabled institutions |

| Average ROI on AI investment | $3.50 per $1 (top: $8) | Accenture Research 2026 | Financial services AI deployments |

| AML alert reduction | 80%+ | Nasdaq Verafin 2025 | Sanction screening agentic AI |

| Operational cost reduction | 35% | Accenture 2026 | AI-enabled financial institutions |

| KYC processing: before AI | 5–10 business days | Industry benchmark | Manual review at major banks |

| KYC processing: with AI | Minutes to hours | Accenture / Kore.ai 2026 | Standard profiles, AI straight-through |

| Loan decision: before AI | 14+ days | Nimble AppGenie 2026 | Manual cross-border loan origination |

| Loan decision: with AI | Minutes | Nimble AppGenie 2026 | AI agent orchestrated pipeline |

| Compliance cost saved | $16M over 4 years | Fenergo case study | Regulatory KYC process automation |

| ROI payback period | 6–9 months | Ampcome / Kore.ai 2026 | Most implementations |

| KYC simple implementation | 4–6 weeks | Ampcome 2026 | KYC expiry tracking use case |

| AML complex implementation | 2–4 months | Ampcome 2026 | Full AML pattern detection deployment |

8. Implementation Roadmap

Based on the implementation timelines reported by Ampcome, Kore.ai, Nimble AppGenie, and FIS, here is the realistic roadmap for deploying AI agents in a cross-border loan operation:

- Phase 1 — Data Foundation (Month 1–2): Centralise and clean customer data across all jurisdictions. This is the non-negotiable prerequisite: AI delivers value only when it operates on clean, structured, well-governed data. Establish data residency controls for each jurisdiction’s regulatory requirements — EU GDPR, India DPDPA, Brazil LGPD, and local equivalents.

- Phase 2 — Pilot Use Case (Month 2–3): Start with the highest-ROI, lowest-risk agent: KYC expiry tracking and document completeness monitoring. Simple monitoring use cases can be operational in 4–6 weeks. This builds institutional confidence, establishes governance frameworks, and produces measurable ROI before expanding to higher-stakes agent deployments.

- Phase 3 — KYC & AML Agents (Month 3–6): Deploy the KYC and AML agents for new applications. Configure explicit confidence thresholds: high-confidence, low-risk applications move through straight-through processing; applications below threshold route to analysts with full AI-generated context. Document all model decisions, confidence scores, and escalation triggers for regulatory audit readiness.

- Phase 4 — Credit Risk & FX Agents (Month 4–8): Integrate credit risk assessment with existing underwriting systems and cross-border bureau connections. Deploy the FX agent with conservative hedging thresholds initially, expanding automation parameters as performance data accumulates. Validate all models against historical data before production deployment.

- Phase 5 — Compliance Reporting Agent (Month 6–9): Deploy regulatory circular monitoring and automated reporting. Start with one jurisdiction, validate output quality against manual review, then expand. Ensure all AI-generated compliance reports include full audit trails and human-readable explanations before submission to any regulator.

- Phase 6 — Full Pipeline & Servicing Agent (Month 8–12): Integrate all agents into the unified orchestration layer. Deploy the loan servicing agent for ongoing portfolio monitoring. Establish continuous performance monitoring with defined drift detection thresholds — static models degrade over time and must be retrained as market conditions and regulatory environments evolve.

| ⚠️ Compliance AlertRapid adoption can lead to unsanctioned AI tools being deployed outside official governance frameworks — building compliance gaps that are hidden until something goes wrong. Every AI agent in a regulated financial workflow must have: documented use case scope, risk classification, named ownership, testing records, confidence thresholds, fallback rules, and review triggers. These controls are non-negotiable in 2026’s regulatory environment. |

9. Frequently Asked Questions

What are AI agents for cross-border loans?

AI agents for cross-border loans are autonomous AI systems that manage end-to-end international lending workflows — including application intake, KYC identity verification, AML transaction monitoring, credit risk assessment, FX hedging, regulatory compliance reporting, and loan servicing. Unlike rule-based automation, they plan, decide, and execute multi-step workflows across jurisdictions with minimal human intervention, with human escalation triggers built in for complex or high-risk cases.

How much do AI agents reduce cross-border loan processing costs?

Financial institutions using AI agents for cross-border operations report 35% reduction in operational costs on average, with top performers achieving up to 55% efficiency gains, per Accenture 2026 data. The average ROI is $3.50 per $1 invested in AI, with top performers reaching $8 per dollar. Most institutions see measurable ROI within 6–9 months of deployment. Fenergo documented $16 million in regulatory compliance cost savings over four years from KYC automation alone.

What regulations govern AI agents in cross-border lending in 2026?

The key regulatory frameworks in 2026 include: the EU AI Act (mandatory from August 2, 2026 — requires transparency, audit trails, and explainability for high-risk AI in financial services, penalties up to €35M); EU AMLA (direct supervision of high-risk cross-border financial entities, single rulebook enforcement); FATF guidelines (73% of jurisdictions now have Travel Rule legislation); FinCEN/BSA requirements in the US; Australia’s Tranche 2 reforms effective July 2026; and India’s DPDPA and Brazil’s LGPD for data handling.

Can AI agents fully replace human compliance analysts in cross-border lending?

No — and regulators explicitly require they do not. The defensible model in 2026 is bounded autonomy: AI agents handle routine, structured, high-confidence tasks autonomously while routing complex cases to human analysts with full AI-generated context. Source of funds reviews, complex UBO analysis, high-risk geography reviews, and adverse media relevance checks still require analyst interpretation. The EU AI Act and FATF guidelines both require human oversight mechanisms for high-risk financial AI decisions.

How do AI agents handle FX risk in cross-border loans?

AI FX agents monitor exchange rates across all relevant currency pairs in real time, execute hedging actions automatically when pre-defined thresholds are breached, recalculate EMIs and repayment schedules in borrower-currency terms continuously, and generate multi-currency statements in local languages. The ISO 20022 messaging standard enables this automation at global scale by providing the rich structured data that AI agents need to automate sanctions checks, fraud detection, and reconciliation across currencies.

What is the biggest risk of using AI agents for cross-border loan compliance?

The cascading error risk: in multi-agent architectures, an error made by one agent becomes the input for the next, building a chain of flawed decisions that is difficult to trace. A KYC agent that misinterprets a rule can feed inaccurate data to an AML agent, creating a compliance gap that is hidden until a regulatory review. The mitigation is governance-by-design: every agent must produce documented reason codes, confidence thresholds, and audit trails — and human review must be triggered at defined escalation points, not only at final output.

10. Conclusion & Key Takeaways

AI agents for cross-border loans are not a future fintech trend — they are the current operational reality for institutions competing in the $4.3 trillion global cross-border lending market. The performance data is unambiguous: 52% fewer processing errors, 38% faster transaction completion, loan decisions in minutes instead of 14 days, and $3.50 ROI per $1 invested. The regulatory environment is equally clear: the EU AI Act enforcement from August 2026 makes explainable, auditable AI architecture mandatory — not optional — for any institution using AI in credit decisions, fraud detection, or AML compliance.

For fintech companies and traditional lenders entering cross-border markets in 2026, the strategic choice is not whether to deploy AI agents — it is how to deploy them responsibly. The institutions that will win are those that build compliance and explainability into their AI architecture from day one, implement bounded autonomy with clear human escalation triggers, and treat regulatory governance as a competitive edge rather than a compliance cost.

4 Comments

Pingback: 15 Best Agentic AI Tools & Platforms for Autonomous Agents 2026

wish you best and best

AI xeberleri iqtisadi xeberler

Thank you for taking the time to share your thoughts! We truly appreciate the support and are glad you found value here. Stay connected—there’s more helpful content coming your way.